The Basics of Business Financial Accounting

Financing a business sounds very difficult. While ‘easy’ is not a word to throw around when you’re investing in a business, I will say it’s not as difficult as it seems. The problem with investing in your business is that commercial ventures usually have big bad words attached to them. Scary words like accounting, loans, debt, bankruptcy, and settlements. If you are a commerce graduate, you’re probably not scared of them that much, but why are they so scary to everyone else! Whoever made them needs to be put on trial. Anyway, coming back to financing a business, let us jump into it without wasting too much time. You’re in for a long blog. Read on!

Anyway, coming back to financing a business, let us jump into it without wasting too much time. You’re in for a long blog. Read on!

Part 1:

Initial Funding

Small Business Loans

Venture Capital

Basic Financial Accounting

Debt Management

Avoiding Bankruptcy

Part 1:

Initial Funding

The most important aspect of running any business is its funding. Unless you’re someone living in the richest suburbs of the world, capital is something you will need to worry about. And a business can be a black hole for money if you are not careful. You can watch the video given below to learn more about the various strategies on how to fund a business.(Above video is a part of a more elaborate course on Academy by Appy Pie. To access the complete course, please Click Here, or continue reading below.) There are various ways to fund a business. Let us discuss some popular tried and tested options.- Bootstrapping Bootstrapping is essentially funding your business by yourself. You can use your own money from your savings, debt (credit cards and personal loans). You can self-fund by selling your assets such as your house, or estate, etc. Once your business kicks off, you can use the profits from your sales to generate growth for your business. Bootstrapping or self-funding is successful only if you are careful and have a business idea that has a fast growth rate. If your idea succeeds bootstrapping is the most profitable way to run a new small business.

- Family & FriendsAsk people around you to help you. Your family and friends can fund you and it is never a bad idea to get yourself funded by them. However, if your business fails, repaying them will be a big issue. Spoilt relations will hurt you more than a failed business. Be careful before asking your closest ones to invest in your idea.

- Angel InvestorsBefore I explain, don’t let the word ‘angel’ fool you. Angel investors are rich people looking to invest in an idea. They invest in new businesses hoping to make a profit in the future. While angel investors are a relatively low-risk option for early investments, but be careful while negotiating with them. They will hate me for saying this, but angel investors can often take control of someone else’s businesses legally. It’s not surprising that some business owners get thrown out of it. Read every line before signing any agreement with them. Watch out and protect your business and your stake in it at all costs.

- CrowdFundingCrowdfunding is a relatively new way to work towards an idea. It usually involves securing funding from people. However, crowdfunding is only popular for a business that can emotionally move the masses or provide value to many people. The greatest disadvantage of crowdfunding is that once you collect the funding you owe hundreds, maybe thousands of people. If your final product isn’t as good as people expected, you’re in for a fall from grace.

Small Business Loans and Venture Capital

Say, your initial funding is successful. Your business started growing and is now fairly established over a certain area. The next phase for your business is to grow and generate revenue & profits. Growing a business will go well at first, but it will eventually hit a wall. Profits alone won’t be enough to help it grow. A business needs investment to grow. Once that happens with your business, you could go public with your business and trade it on the stock market. However, small businesses have a hard time securing funding in the markets. This leaves two ways to generate growth in your business.Timeline for the loans can be extended.

Specific projects can be financed, R&D can have a loan without needing to compromise marketing, sales, etc.

Allows you to keep ownership of your company (Look at Venture Capital).

Can be used to finance a purchase. Example: A new office block.

Small Business loans take precedence. You pay it off first and later use your profits for other activities. It is also called senior debt.

Only suitable for a business going through a phase of hyper-growth. If your business is growing slowly, you will face a problem paying it back.

Missing your payments will give you a bad day. Missing too many payments will lead to the institution freezing your assets.

It can affect the owner’s credit score. Goodbye, new Porsche! Since small business loans can have higher interest rates, another potential way to fund your business is to take a personal loan from your individual credit. To know if it is a good idea, you can watch the following video:

(Above video is a part of a more elaborate course on Academy by Appy Pie. To access the complete course, please Click Here, or continue reading below.)- Venture capital does not require you to pay back the investment. It’s essentially the other party gambling on your business.

- Venture capital brings quick growth for your business and gives you investment opportunities.

- It can help you network better and put you in touch with established businesses.

- Venture capitalists get a stake in your company with which you can lose your freedom to choose how things go.

- Your company may fail to grow, and you may have to incur the most loss.

- It is harder to raise funds through capital unless you have good networking.

Small Business Loans

There are various institutions out there, ready to give your business a loan. I should let you know small business loans are also known as venture debts. See! Scary words are common in the business world. Coming to business loans, organizations like banks, hedge funds, private firms, business development companies (BDC’s), etc. Venture Loans are a great way to grow your business. The usual payoff period is around 3-5 years. Here are the pros and cons of small business loans.ProsVenture Capital

Venture Capital is a form of private equity. In Lehman’s (pun intended) terms, venture capital is an investment in your business by wealthy investors, financial institutions, and investment banks. This option is limited to businesses which have a long-term growth likely to support them. Venture capital is a risky move for said parties, but the end payoff is an attractive offer. Venture capital can be equated with angel investing for new businesses. Here are the pros and cons of venture capital.ProsPart 2:

Basic Financial Accounting

Financial accounting helps you keep track of your organization’s financial transactions. These observations are recorded, summarized and presented in the final report to analyze the performance of a company. Financial accounting provides an idea of how valuable is the company. Note that the true value of a company cannot be deduced from financial reports but rather it serves to provide a rough idea of a company’s financial strength. Given below are a few basics of financial accounting.- Double Entry Accounting

- Accrual Basis of Financial Accounting

- Why You Need Financial Accounting for Your Small Business

- Calculating profit

All financial accounting is done with double-entry bookkeeping. This means that all financial accounts are compiled while keeping in mind both credit and debit.

A little difficult to understand, the accrual basis of financial accounting is a form of accounting where transactions are reported according to the time they happen and not when they are paid or received. In simpler words, you write transactions as they happen. For example, you sold a book for 10$ on credit. You will write it in your financials as soon as you sell not when it is paid off. This is standard practice for all businesses that average over $5 million annually.

Combining these two principles you can maintain your financials. Various financial statements can be generated from financial bookkeeping. Now, I will not be discussing the kinds of financial statements in this blog. That deserves a blog of its own.

You can learn more about financial accounting and how to set up your financial books from the following video.(Above video is a part of a more elaborate course on Academy by Appy Pie. To access the complete course, please Click Here, or continue reading below.)

You must be wondering that your new business is small, so does it really need financial accounting? Why do you need to complicate it right now? Here’s the catch. The moment you try to secure a loan or capital for your business, your business’s financials will come into question. If you don’t have a history of good finance recollection behind you, it will become difficult for you to get a good deal that can benefit you. Even investors look at companies with good financial records behind them.

Maintaining a petty cash book or basic accounting won’t help your small business in the long run.

So many profitable businesses lose investors due to shoddy financial practices. Maintain your financials with grit and integrity. In addition, once your business crosses a revenue of $5 million it is almost mandatory for you to maintain your financials. No accountant on the planet will audit your business for you if you don’t maintain your financials. The good news is that it’s effortless to keep financial records in this digital era. Apps like Akounto, Freshbook, etc can easily integrate into your bank accounts.

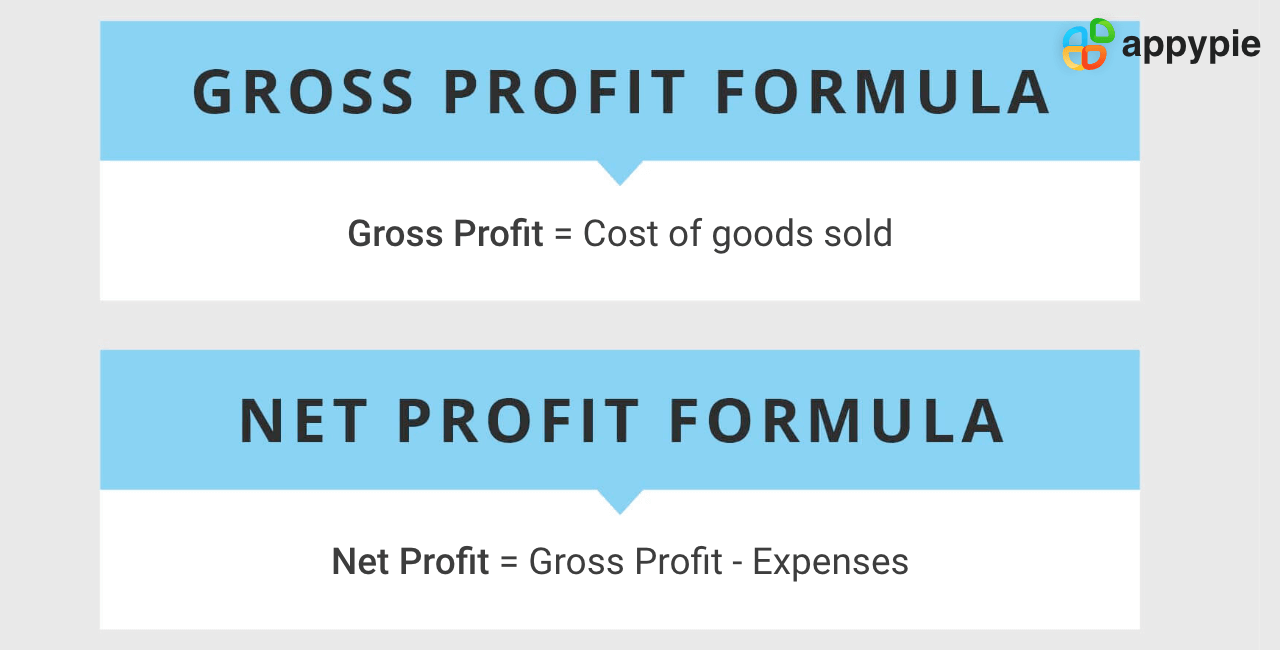

Calculating profit is relatively simple. Your financial statements that will be generated will give you an idea of your revenue. Mind you! Revenue is not profit. Once you have your revenue pinned down, you remove the COGS or Cost of Goods Sold from the revenue. This will give you an idea of your gross profit.

You can then remove the expenses from your gross profit to calculate your net profit or net income. The expenses are usually manufacturing, production, salaries, etc.

Debt Management

Now we come to an important part of this blog. In my opinion, this is perhaps the most important. No matter how good your business idea is or how successful it gets, you will have to either take a loan or divert it to investors to grow. That is just how a business grows. Even if you go public and plonk your companies through IPOs you technically still are in debt. If you don’t manage your financials right, you will have a hard time avoiding extreme losses or even worse, declaring bankruptcy. You need to ensure that you have a steady influx of cash and can manage a business without too much debt. Business debt is a horrifying thing and can create a domino effect that can eventually reach your end customer. To keep the ship sailing, you need to manage your debt. There are various companies out there that will help keep your debt in check by dealing with the creditors and keep your business smooth. But you can avoid them when you’re a smaller business. Consider seeking assistance from a bad debt insurance provider to safeguard your business from potential financial risks.- Make an inventory of your debts:

- Boost sales:

- Cut costs:

- Refinance High-interest debt:

- Maintain goodwill:

- Debt Management:

- Know how much you sell:

- Protect yourself financially:

- Calculate your maximum cost level:

- Tell everyone:

- Hire an expert:

How to Get Out of Business Debt

There’s not a lot you can do if your business is unable to generate enough gross profit to deal with business debt. However, here are a few tips to manage your business debt and keep it in check until sales are boosted:Small business loans are easier to manage if you have an inventory of them. Create a table of all your loans and divide them based on amount and interest. Once you have done this, start dealing with them according to priority. Take out the high-interest ones first.

Marketing, nowadays is affordable. Market the hell out of your products and get those sales. Reward existing customers and be sure to have limited offers to get even more.

Not a recommended solution but cutting costs can help. Remove extra office space. If the situation is bad, downsize. Ask the co-operation of your employees and reduce expenditure on employee comforts. Cutting costs is never a good idea but it does help.

This is possible only if you have a good credit score. In refinancing, you pay off a high-interest debt by taking an equivalent low-interest loan. This helps save crucial dollars in the long run.

The world isn’t as bad as it seems. Maintaining goodwill of employees, customers, investors can go a long way. This is something so many businesses fail to do. You can also watch the video given below to find more tips on how to get out of business debt

(Above video is a part of a more elaborate course on Academy by Appy Pie. To access the complete course, please Click Here, or continue reading below.) Business debt is a cruel thing and managing it is even crueler. Make sure you do it. If you fail, you may have to face bankruptcy.Avoiding Bankruptcy

Bankruptcy is the last thing you would want to do to your business. Here is a simplified tip-list to avoid bankruptcy.How to Avoid Bankruptcy

As explained above, managing your debt is the easiest way to avoid bankruptcy.

Sit down with your sales team and analyze exactly how much you sell. Match your average sale to your debt. Clear your profit margins for the time being and reinvest profit you’ve made in the past to clear the

debt.Don’t reinvest too much. Your business is only as good as you are. Make sure you have an exit strategy if your business fails.

This is calculated by subtracting the monthly debt burden from your average sales and then subtracting net profit from the remaining amount. This amount is the amount you can spend to keep afloat.

Let people and organizations who lent you money know that you’re considering bankruptcy. Ask to restructure your debt. Given your situation, they’re likely to oblige.

Finally, some specialists can help you turn around a business. These people are experienced at keeping businesses afloat. Hire them on a contractual basis. They may just save your business.

Related Articles

- Learning In-Hand Translation Using Tactile Skin With Shear and Normal Force Sensing

- Personalizing for Perfection: A Guide to Handling 20 Types of Customers

- How to Capture Perfect Screenshots on Android: Expert Guide

- Ethics In Artificial Intelligence And Robotics

- Top Harvest Integrations to Supercharge Business Operations

- How to Successfully Grow Your App? – A Quick Guide

- How to Convert Images from JPG to JPEG Format?

- Best Strategies For Making An Ideal Weekly Plan Schedule

- How To Create Customer Feedback Chatbot

- How to Install Windows 11 from an ISO File: A Complete Guide

Take a Related Course

- Start learning for free

(No credit card required)

Most Popular Posts

- 25 Best Techniques For Phone Customer Service

- A Beginner’s Guide to Custom Calendar Design

- History of Orange Color in Graphic Design: 25 Best Colors that go with Orange Color

- Web2Code: A Large-scale Webpage-to-Code Dataset and Evaluation Framework for Multimodal LLMs

- How can a LinkedIn Banner Boost Your Business Page?